![[Open Source] Anti-wealth concentration mechanism for web infrastructure](https://cdn.prod.website-files.com/681cd2fafbaa77cf81b77ffc/6940846238d17bf6b292e30a_Screenshot%202025-12-15%20at%204.55.48%E2%80%AFPM.png)

[Open Source] Anti-wealth concentration mechanism for web infrastructure

Subsidy mechanism to (1) minimize incentives to hoard wealth & (2) foster economic conditions supporting smaller providers.

I designed a novel subsidy allocation and distribution mechanism for the Threshold Network, a multi-app digital services platform with hundreds of independent service-providers and tens of thousands of users. To date, the mechanism – dubbed Stable Yield – has distributed over $30m in subsidies over the course of ~3 years. The service-provider population slowly grew without any signs of wealth hoarding in that time period.

The design attempts to offset and counter the non-ergodic, path-dependent properties of economies with unevenly spread wealth, that is, the 'rich-get-richer' effect. This dynamic is highly conspicuous in the real economy, and indeed is exacerbated by (deliberately) flawed mechanisms and policies. The R&D also involved quantitative analyses of prevailing subsidy allocation algorithms in decentralized networks, with Stable Yield challenging an orthodoxy amongst protocol designers seeking to regulate service-side participation in two-sided markets. An abridged version of the original proposal is below, along with an introduction from the associated research. See this (very) tongue-in-cheek X thread that attempts to preempt criticism of the mechanism.

Zooming out, here's a more general talk I gave at MIT about designing economic mechanisms to coordinate and incentivize distributed (and pseudonymous) service-providers, centered around the locking of collateral ('stake') and without relying on legal recourse for errant or malicious actions. Or distributed-collateral-based-pseudonymous-digital-service-provider-economies, for short.

Stable Yield Rationale

The number of genuinely economically independent service-providers (hereafter the ‘# nodes’) is a critical measure of the security and utility of virtually all decentralized networks. The modular services/apps hosted on Threshold Network are no exception. However, the # nodes network statistic is only discernible anecdotally/trustfully (i.e. not currently verifiable via consensus). Moreover, attempting to maximize the # nodes directly via the protocol remains an ill-advised strategy, lest the mechanism fall prey to Sybil-style manipulation. An often overlooked and measurable network statistic is the break-even collateral size – the minimum sum of tokens a service-provider must lock to avoid operating a loss at a given timestep. The volatility of the break-even collateral size, and how close it stays to the minimum collateral invariant, are major determinants of the theoretical number of service-providers that are capable of surviving and thriving as the backbone of a decentralized digital service.

Many protocols target a participation rate (percent of total circulating token supply locked as collateral) as a proxy for optimizing the # nodes, dividing a fixed reward ‘budget’ amongst a fluctuating array of active providers. Some go further by engineering a second-order variance via the nominal inflation rate (Cosmos, Livepeer, ETH2). Both these designs foster conditions that may actually further centralization trends over the medium/long-term. Elevated staking rates and correspondingly low yields do little to persuade deeper-pocketed service-providers to scale back capacity, but do

(a) debilitate non-Institutional (smaller) provider balance sheets

(b) increase the ‘subsidy hoarding’ payoff for those who can afford it.

The combination of dynamics (a) & (b) can engender detrimental feedback loops and widen the gap in fractional token/subsidy share between large and small. This wealth concentration trend eventually diminishes the # nodes. See Subsidization & Participation Bivariate Analysis notebook for a deep-dive on this issue, and the driving empirical evidence behind this proposal.

Stable Yield Mechanism

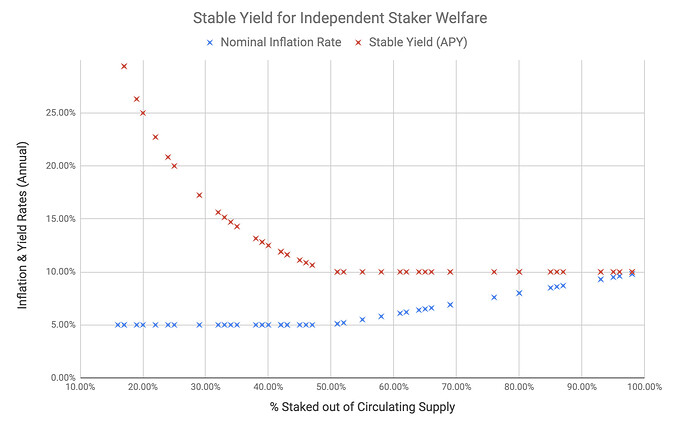

The proposed mechanism minimizes + stabilizes the break-even stake size by programmatically adjusting the nominal inflation rate – thereby targeting a minimum effective yield to all service-providers, independent of fluctuations in the participation rate or number of active providers from timestep-to-timestep. The mechanism confers economic sustainability by being greater than or equal to a minimum target rate, and encourages longer-term financial planning via lower variance in said rate. The Stable Yield is set to a target rate of 15% APY. This, along with other parameters, can and should be modified by the Threshold DAO to accommodate complementary reward models (e.g. buyback-and-distribute), or to tune the (now more variable) dilution burden placed on passive token-holders.

Since non-institutional and smaller service-providers are adversely affected when participation rates are elevated – i.e. when yields are unsustainably low – the proposed mechanism only stabilizes the yield when participation is above a DAO-selected threshold. Below this threshold, the yield is inversely proportional to the staking rate, as is typical in prevailing reward mechanisms. This participation parameter is provisionally set to 50% of the circulating supply.

Context: The Prevailing 'Variable Incentive' Model

Proof-of-Stake (PoS) realizes Sybil resistance by exclusively allocating validation work, and corresponding compensation, to service-providers who have locked non-trivial sums of value (hereafter stakers). Game theoretic devices, which coordinate, mediate and penalize stakers, are built upon this eligibility prerequisite of provably committed capital. Heir apparent to energy-inefficient predecessors, Proof-of-Stake protocols have recently come under increasing academic scrutiny – including the mechanisms which incentivize staker participation, and the long-term economic outcomes of flawed reward allocation functions in particular. PoS rewards are typically generated by minting new units of the network’s native token and distributing them exclusively to active stakers. This implies that the reward's value is contrived via the dilution of token holdings belonging to non-recipients. The percentage that the circulating token supply is expected to grow per year, through the issuance of new tokens as rewards, is commonly referred to as the nominal inflation rate (I_nom).

The central focus of this study is what we describe as the variable incentive model. At any given instance of reward generation and issuance, the size of the reward received by any one staker (and their delegators) varies based on the percentage of tokens staked out of the entire supply in that instance – the staking rate (S_rate). The staking rate reflects the total capital commitment to the network by stakers (including tokens committed indirectly by delegators), and ostensibly, the total capacity for service provision. Since tokens distributed as rewards are not immune from dilutionary effects, calculating the 'true' value of the reward must also take this into account. We may now construct an expression for a reward's true value in a given instance, referred to as the real yield (Y_real). The real yield can be summarized as the annualized percentage growth of an arbitrary staked holding of tokens, that has been modified, via the equation below, to reflect its true value at each timestamp.

Y_real = I_nom/S_rate - I_nom

The variable incentive model is far from an unavoidable, reluctantly accepted design flaw. Rather, the inverse relationship between staker participation (i.e. the staking rate) and true reward value is an attempt to programmatically regulate service-provider participation within expedient bounds. An implicit assumption that underpins this model's design is that stakers' heuristics/preferences prioritize returns over short-term horizons, and bond/unbond tokens on a frequent basis. A loose analogy for this class of rational agent are day-traders (as opposed to value investors), who not only pay greater attention to ephemeral indicators and deviations, but act upon them. With variable incentives, the supposed rational reaction to observing a period with relatively high real yield is to commence staking with passively held tokens or increase the size of an existing stake, amongst prospective and active service-providers respectively. Equally, the model assumes the rational reaction to a period with relatively low real yield is to reduce the size of an existing stake or cease staking altogether. In this way, the variable incentive model is designed to balance and moderate the staking rate.

One may infer this rationale, and underlying assumptions, from the proactive modification of certain reward mechanisms, which effectively double-down on the principle of the variable incentive model. Though the exact parameters are different, the Proof-of-Stake networks Cosmos, Livepeer and Ethereum 2.0 utilize mechanisms that adjust the total reward budget (nominal inflation rate) in response to a fluctuating staking rate. Instead of expanding the reward budget in response to greater participation, which would resemble a traditional subsidy model, the exact opposite is enforced. When participation rises beyond a fixed target rate (66.7% and 50% of the circulating supply for Cosmos and Livepeer, respectively), the total reward budget decreases, and vice versa. In Ethereum 2.0's case, there is no explicit target staking rate, but the current leading proposal for reward design advocates maximum network issuance as an inverse function of the total sum of tokens staked. In all cases, this design further increases the dependence of the the true reward value on the collective, day-to-day (or block-to-block) decision-making of active stakers/delegators, dormant stakers/delegators and passive token-holders, with respect to their staking activity.

The staking rate, and its evolution/volatility over time, are imperfect but critical public indicators of network stability, diversity and staked wealth. Thus, protocol designers seek to influence the staking rate and maintain it within expedient bounds. The upper and lower bounds of expediency are not formally identified or quantified in network documentation, but there are clear problems with both extremes. The dangers of a depressed staking rate are well documented; undermining network stability, diversity and staked wealth, any of which increase vulnerability to potentially fatal collusion attacks. Elevated staking rates are unlikely to engender as catastrophic an outcome as the opposite extreme, but create conditions for deep-seated and potentially irreparable problems to emerge over the long-term. Firstly, when the vast majority of native tokens are staked, this limits the availability of the token. Prospective network users, who must acquire the native token and use it to pay fees, encounter the dual frictions of low liquidity and associated volatility. Secondly, it has been argued that a predominant tendency for token-holders to lock their tokens for indefinite time frames ('stake hoarding'), when combined with a fixed, finite token supply, can contribute to deflationary forces. Deflation, or even the spectre of it, not only stymies the native token's utility as a payment token, casting it as an asset rather than a currency, it also reinforces the expected utility of holding the token for extended time frames – encouraging further stake hoarding.

Further undesirable dynamics may occur with respect to the composition and behavior of the staker array, given that perennially elevated staking rates are a form of market oversupply. Because rewards (and transaction fees) are divided up amongst all active stakers, an oversupplied network will fail to sufficiently support and subsidize some stakers' operations. The stakers most likely to survive periods of chronic oversupply, and deficient compensation, are those with the greatest resources at their disposal. Crucially, market oversupply is not necessarily self-correcting. A dip in the real yield can conceivably induce a corresponding rise in the staking rate, as stakers rich and poor attempt to increase their fractional share (and commensurate rewards), to make up the loss. Oversupply, wealth concentration and detrimental feedback loop dynamics are explored in the full study.

Latest Projects

All Projects

![[Teaching] Lecture series on decentralized public goods at Amrita University](https://cdn.prod.website-files.com/681cd2fafbaa77cf81b77ffc/68ab7b8d6f57c49b9d092f6b_Screenshot%202025-08-24%20at%204.52.14%E2%80%AFPM.png)

![[Teaching] Lecture series on decentralized public goods at Amrita University](https://cdn.prod.website-files.com/681cd2fafbaa77cf81b77ffc/68dd9105cc9572763d51e3ec_Screenshot%202025-10-01%20at%204.37.17%E2%80%AFPM.png)

![[Policy] Anonymity-preserving 'smart' channel for reporting antitrust violations to the FTC](https://cdn.prod.website-files.com/681cd2fafbaa77cf81b77ffc/68dffbf2b6d55ae97c256eb4_Screenshot%202025-10-03%20at%2012.37.14%E2%80%AFPM.png)

![[Policy] Anonymity-preserving 'smart' channel for reporting antitrust violations to the FTC](https://cdn.prod.website-files.com/681cd2fafbaa77cf81b77ffc/68ead19b7d54025b3c502d49_Screenshot%202025-10-11%20at%205.52.12%E2%80%AFPM.png)

![[Policy] Eliminating ‘Lender Lock-in’ for SBA-Guaranteed Loan Applicants](https://cdn.prod.website-files.com/681cd2fafbaa77cf81b77ffc/68b3334cb07856dcd86fc5f8_948f5670d1acb8a69a4f94ab9460a422.jpg)

![[Policy] Eliminating ‘Lender Lock-in’ for SBA-Guaranteed Loan Applicants](https://cdn.prod.website-files.com/681cd2fafbaa77cf81b77ffc/68dd906bd699b79a56586cfb_Loan.png)